Is Tax Reform Possible?

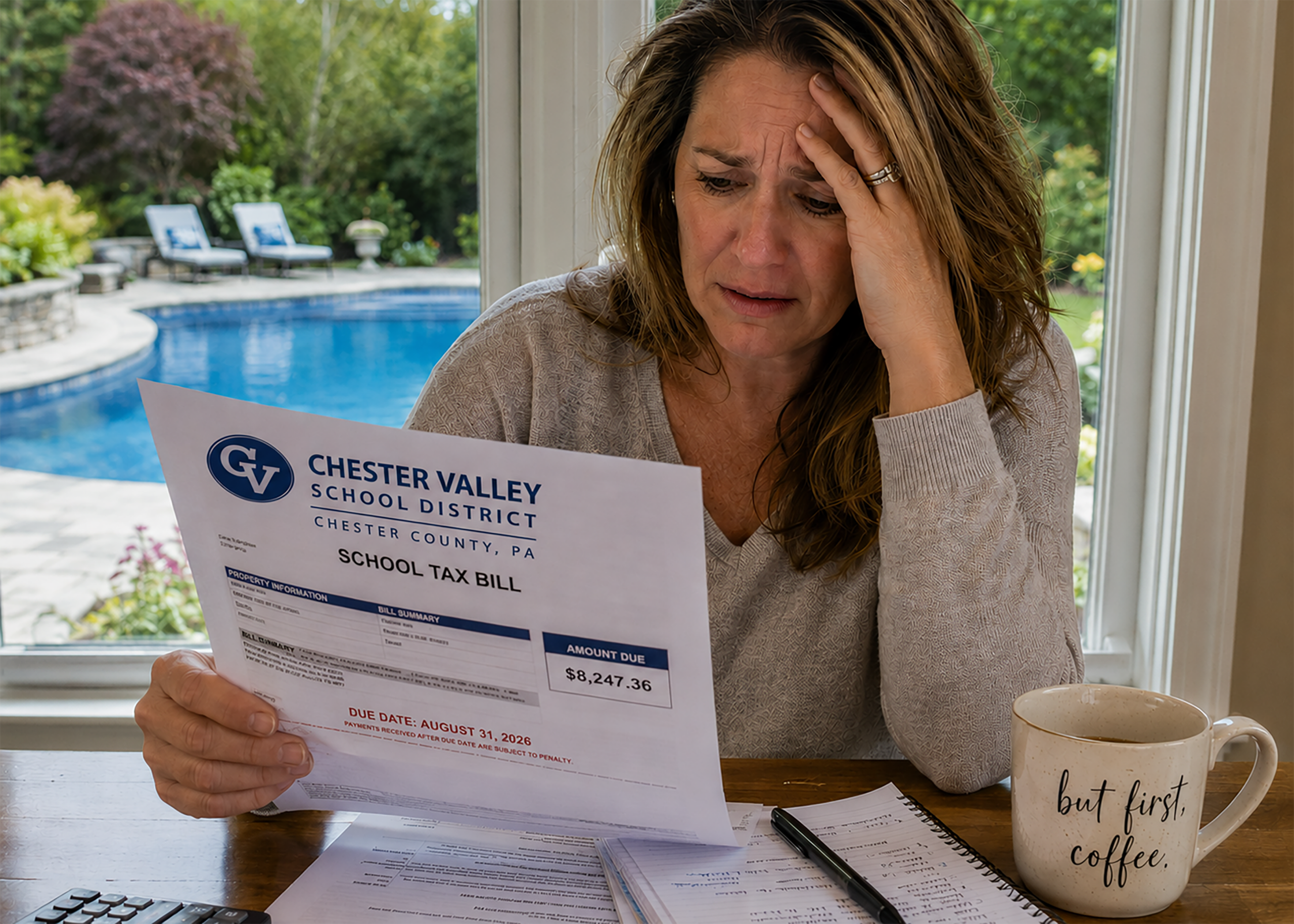

As summer approaches, you look forward to weekends at the shore, sunny days in the pool, and relaxing vacations. Just as you start to decompress and enjoy the warm weather, the school real estate tax bill arrives and the relaxation comes to a screeching halt!

No matter a person’s age or economic status, if you are a property owner or renter, then you cannot escape paying those school real estate tax bills. Renters often don’t realize that the property owner passes those real estate tax costs onto the tenants as part of the rent or common area maintenance charges.

With ever-increasing property valuations and mostly stagnant or slower growth incomes, many property owners find it difficult to pay taxes based on the property values. Additionally, school board budgets rise year after year.

According to the Commonwealth Foundation, enrollment in public elementary and secondary schools has declined by 300,000 students over the past 25 years. Yet, anyone who has lived in and paid taxes on the same residence, consistently for several years, can attest that those school real estate taxes NEVER decline despite decreasing enrollment.

How is it possible that taxes never decrease? Why are budgets growing every year? Can’t anyone come up with a better and fairer way to fund our schools? Some legislators believe they can.

Hold Harmless

Although property values and, more specifically, assessed values are involved in calculating school real estate taxes owed on a property, they are not the primary reasons taxes do not decrease from one year to another. Instead, a main reason school budgets and resulting taxes never drop is because of a “hold harmless” provision in Act 85 of 1992 regarding PA education funding.

The term “hold harmless” is a legal phrase that “refers to a contractual provision in which one party agrees not to hold another party liable for certain losses, damages, or claims that may arise from the performance of the contract,” according to Cornell Law School.

The state’s hold harmless provision is essentially part of an education contract between the state and school district that was encoded into legislation. That contract does not hold a school district liable for losses in student population, for damages for student learning losses, or for claims arising from decreasing proficiency performance in test scores. There is no liability or claim against a school district’s funding if students leave the district or they are not proficient in English or Math. No, in fact, legislation prescribes that each school district must receive at least as much state funding as it received the prior year. The student population drops by 1,000? Same funding. Proficiency rates for English and Math are 40%? Same funding.

Generally, local school tax revenue pays for anything not funded by the state or federal government. When a school district knows it will receive at least the same state funding each year (plus annual upward adjustments) despite any changes in student population, then why would it decrease its budget? Costs of salaries, healthcare, and pensions for administrators, teachers, aides, specialists, etc. usually increase each year. School districts can set the local tax rate (within state limits) to pay for the cost increases and additional projects not covered by guaranteed state funding. Property owners must pay. That’s it.

NOTE: The PA Department of Education provides a synopsis of basic education funding and discussed the history of the hold harmless provision in this 2023 document.

School Property Tax Elimination Act

On May 29, 2026 PA Sen. Dawn Keefer joined The Conservative Voice on WWDB 860AM to discuss and explain the legislation that she introduced to eliminate school real estate taxes across Pennsylvania. It is known as the School Property Tax Elimination Act or S.B. 962.

A key component of this legislation makes school districts financially accountable for the tax dollars entrusted to them. School districts that are unable to stay within their budgets under the new structure would be given an advisor to help with the financial management. If a district is still unable to manage its budget after one year, then it would be dissolved and its schools merged into surrounding school districts.

Local school real estate taxes currently generate $17.5 billion in income across the Commonwealth of Pennsylvania. This bill aims to use a less regressive tax structure to supply the same income to school districts throughout the state. Sen. Keefer understands the concerns of residents who are at risk of losing their homes or farms due to the inability to pay the increasing school taxes.

The shift in income sourcing would come in the form of two tax increases: sales tax and personal income tax increases.

Sales Tax

Under this plan, the PA sales tax would increase 2% on currently taxed items and a new 2% sales tax would be placed on clothing, candy, and gum. These taxes would go directly to the counties for distribution to the school districts on a per pupil enrolled basis, as opposed to being lumped into the state funding. Apportioning the income to follow the students guarantees that if students move, then the tax dollars follow them to the new school district rather than staying with one with fewer students.

Personal Income Tax

Also, this legislation increases the personal income tax by 1.88%. The tax would be collected by a local collection agency, such as Keystone Collections Group or Berkheimer, and distributed directly to the school districts. All income would be subject to this personal income tax, including withdrawals from pensions and retirement funds which aren’t currently taxed in PA. Social Security, Roth IRA’s, military pensions, or retirement accounts that replaced Social Security deposits would not be taxed. Taxes would be paid on capital gains in retirement accounts, not on contributions made with post tax dollars.

Sen. Keefer understands that seniors are concerned about the taxation of retirement funds. However, many retirees use these same funds to pay school real estate taxes, so she sees it as a swap since school real estate taxes would never come back.

To see how the School Property Tax Elimination Act would impact you personally, click here.

Bottom line…

Pennsylvania school boards are authorized to set tax rates without first getting the approval from voters. Community home values are often seen as an unlimited checkbook for funding school districts either through direct taxation or as collateral for debt for their potential taxation.

Although the School Property Tax Elimination Act does not end the hold harmless state funding provision or make schools immediately accountable for educational outcomes, closing the taxpayers’ unlimited checkbook to the school districts is a start. Putting the choice to purchase items and pay a sales tax that is apportioned according to the needs of the students within each county empowers residents. Pennsylvania is one of only five states with a personal income tax that exempts retirement distributions from taxation. Paying tax on those retirement funds would definitely be a hard pill to swallow for many seniors. The concern that some may have is that once a tax is imposed, it can usually be increased or expanded.

The School Property Tax Elimination Act can be viewed as having positives and negatives about it. It does solve the school real estate tax problem, but there is some uncertainty about future taxes. It’s not all good and not all bad. Perhaps it’s the best kind of legislation, where people meet in the middle and compromise to create a better outcome for all.

As the Constitutional Convention ended in 1787, Benjamin Franklin was asked if the delegates produced a monarchy or a republic. Franklin replied, “A republic, if you can keep it.”

We are trying to keep this republic that we love and hold our representatives accountable to the people. Join us in that mission and share this Update with your contacts!